Hyperliquid investment thesis

An investment thesis for perpetual DEX Hyperliquid using the Sequoia Capital investment framework

Abstract

Hyperliquid is a non-custodial exchange that offers the trading of perpetual contracts. The exchange has facilitated $55.6b in trading volume since its inception in 2022, with $23.7b of that volume occurring in the last 30 days alone. This makes it the 2nd largest derivatives protocol by trading volume over the past 24 hours, surpassing longstanding competitors such as GMX and Vertex Protocol. Despite this, Hyperliquid remains dwarfed by the larger decentralized perpetual exchange (DEX) dYdX, and centralized exchanges (CEXs) such as OKX and Binance.

Table of contents

1. Background

1.1 What is a perpetual exchange?

Perpetual exchanges facilitate the trading of perpetual futures contracts, the single most popular trading instrument in crypto. Since the introduction of XBTUSD perpetual futures by Arthur Hayes, BitMEX co-founder, in 2016, perpetual futures have become an irresistible attraction for crypto traders. [1] The popularity stems from the leverage these contracts offer combined with their time-resilient exposure to cryptoassets.

Perpetual exchanges can be largely categorized into two groups - (1) DEXs such as Hyperliquid and dYdX which are built on blockchains, and (2) CEXs such as OKX and Binance which do not operate on blockchains (but may have separate products that do).

1.2 How do perpetual DEXs work?

There are two major types of perpetual DEXs - (1) automated market makers (AMM) and (2) order books. In AMMs, traders borrow and trade against rely on liquidity pools provided by liquidity providers. On the other hand, order book trades operate similarly to CEXs with clear bid-ask orders. Orders are matched by an offchain matching engine and settled onchain afterward, as order books are generally too computationally intensive for blockchains.

1.3 Why are perpetual DEXs important?

DEXs allow for the leveraged speculation of digital and real-world assets alike. Traders can use these exchanges to make bets on the volatility of an asset. Recently, DEXs such as Hyperliquid and Aevo have also been used for the price discovery of tokens before they even launch, by allowing users to speculate on a representation of the new tokens (i.e. JUP or DYM).

1.4 When did the perpetual DEX market emerge?

Perpetual DEXs emerged in late 2019 with dYdX, the current market leader based on trading volume. Competitors such as GMX and Perpetual Protocol then followed in early 2021. [2]

Figure 1: Monthly trading volumes of perpetual DEXs [3]

1.5 How much in trading volume do perpetual DEXs and CEXs facilitate?

On February 19th, 2024, the 24-hour trading volume across centralized and DEXs was $197b. [4] Only $5.5b of this total volume was driven by DEXs, indicating a large skew towards their centralized counterparts. [5]

2. Purpose

Hyperliquid aims to combine the best elements of DEXs (self-custodial) with those of CEXs (superior trade execution and user experience) into one perpetual trading platform.

3. Problem

The problems with the current perpetual trading landscape can be broadly categorized into two types:

3.1 Problems with CEXs

CEXs, by nature, take control of a user’s funds once the assets have been deposited on the exchange. In the case of dishonest or inadequate management of funds by these exchanges, all user deposits are at risk. In November 2022, major CEX FTX was revealed to have lost $9b in customer deposits. [6]

It is important to note that a growing number of CEXs are beginning to provide proof of reserves, where all user funds are proven to be cryptographically safe (see OKX’s proof of reserves). [7]

3.2 Problems with DEXs

DEXs generally suffer from three main issues - (1) high fees, (2) low trade execution speeds, and (3) low selection of tradable pairs.

In the case of major perpetual exchange GMX v1, traders are required to pay 0.1% of their total notional volume in fees to open or close a position. [8] Although this cut was lowered to ~0.07% in GMX v2, this is still significantly higher than fees taken by centralized exchanges such as Binance or OKX, where the taker fee rates generally range between 0.02% and 0.05%. [9] [10]

On top of this, DEXs are subject to the structural limitations of blockchains, which are only able to finalize transactions based on the speed of the network itself. On some blockchains where the current transactions per second range from 1-5 seconds, this presents a significant issue for leveraged traders that require pinpoint execution of positions. [11]

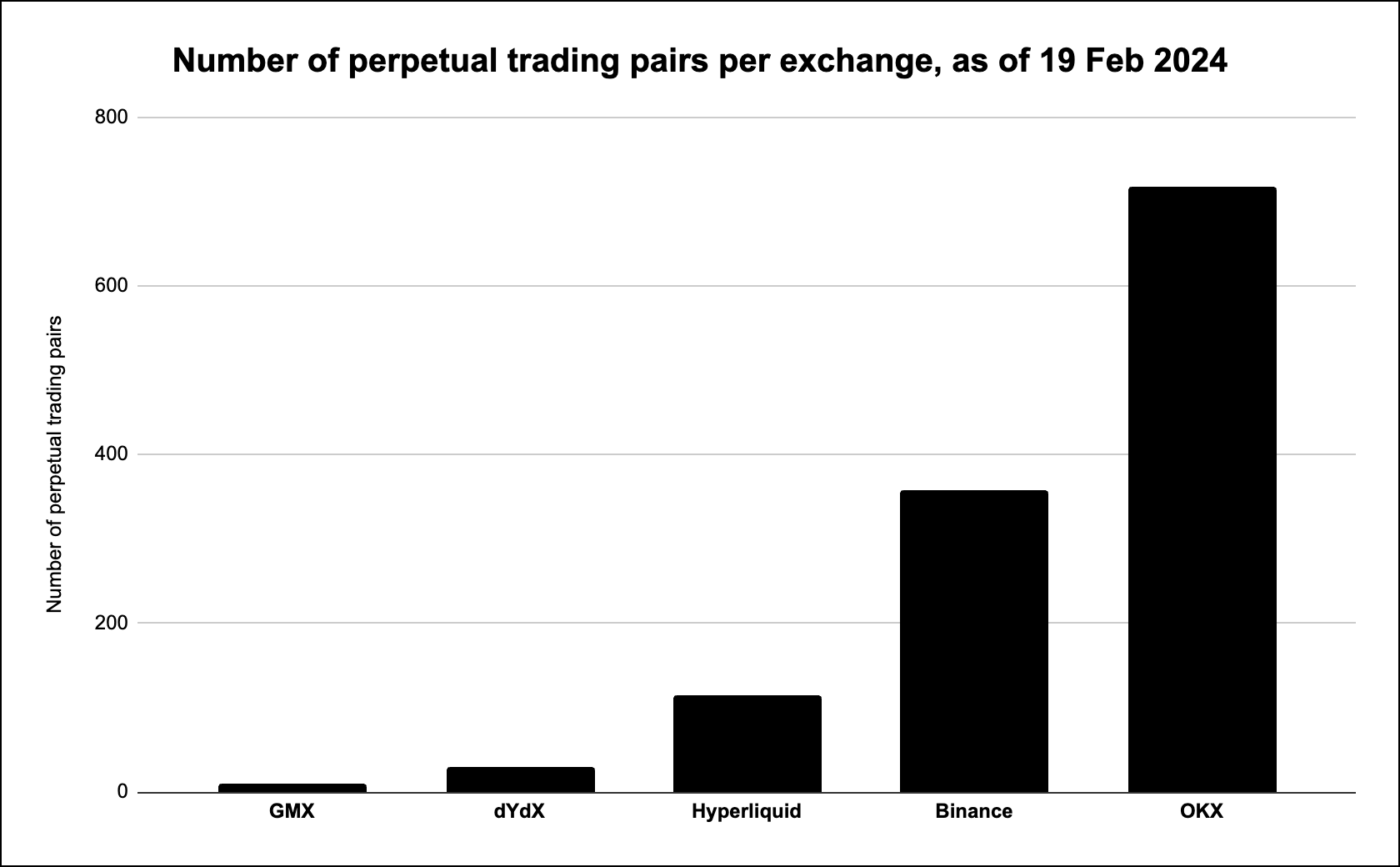

Figure 2: Number of perpetual trading pairs per exchange, as of 19 Feb 2024

The number of tradable pairs for DEXs is also limited, with GMX v2 and dYdX v4 only offering 11 pairs and 29 pairs, respectively. [12][13] This is typically due to the lack of asset price oracles, which are used to fetch reliable asset prices onchain at regular intervals. To put this into perspective, OKX and Binance have over 717 and 357 perpetual pairs available for trading, respectively. [14][15]

4. Solution

Hyperliquid is a perpetual exchange built on its own L1 application-specific chain (appchain) that combines the non-custodial nature of DEXs with the superior user experience of CEXs. At present, Hyperliquid has four main features that have allowed it to gain rapid adoption and become the 2nd largest perpetual DEX by 24-hour trading volume. [16]

4.1 Non-custodial

As user funds are deposited into transparent smart contracts, users retain control over their funds and can easily withdraw assets to the safety of their wallets at all times.

4.2 Low trading fees

Figure 3: Trading fee rates for Hyperliquid [17]

Hyperliquid charges between 0.019-0.035% of notional volume as taker fees, significantly lower than most other DEXs and comparable to CEXs. [18]

4.3 Wide pair availability

Hyperliquid currently supports the trading for 114 assets, an order of magnitude higher than competitors like GMX (11 pairs for v2) and dYdX (29 pairs for v4). This includes innovative pair creation models such as NFTI-USD, allowing traders to bet on an index of the floor prices of major NFT collections. [19] This feature sets Hyperliquid apart from DEX competitors the most in particular, as these exotic pairs are not tradable on other exchanges.

4.4 Fast execution speeds

The Hyperliquid protocol is built on an application-specific blockchain, designed to only run the smart contracts of Hyperliquid. This singular focus allows the Hyperliquid protocol to support up to 20k operations per second. This is opposed to DEXs built on general-purpose blockchains like Ethereum or Avalanche which have multiple protocols running on them, slowing down the trade execution speed for the DEX.

5. Why now?

Both perpetual CEXs and DEXs generally see increased activity when asset prices are volatile, as traders can potentially generate larger profits with less upfront capital. As prices of tokens have increased significantly across the board over Q4’23, open interest (total value of unsettled positions) on CEXs/DEXs have also surged in USD terms.

Figure 4: BTC open interest and volume across major CEXs and DEXs [20]

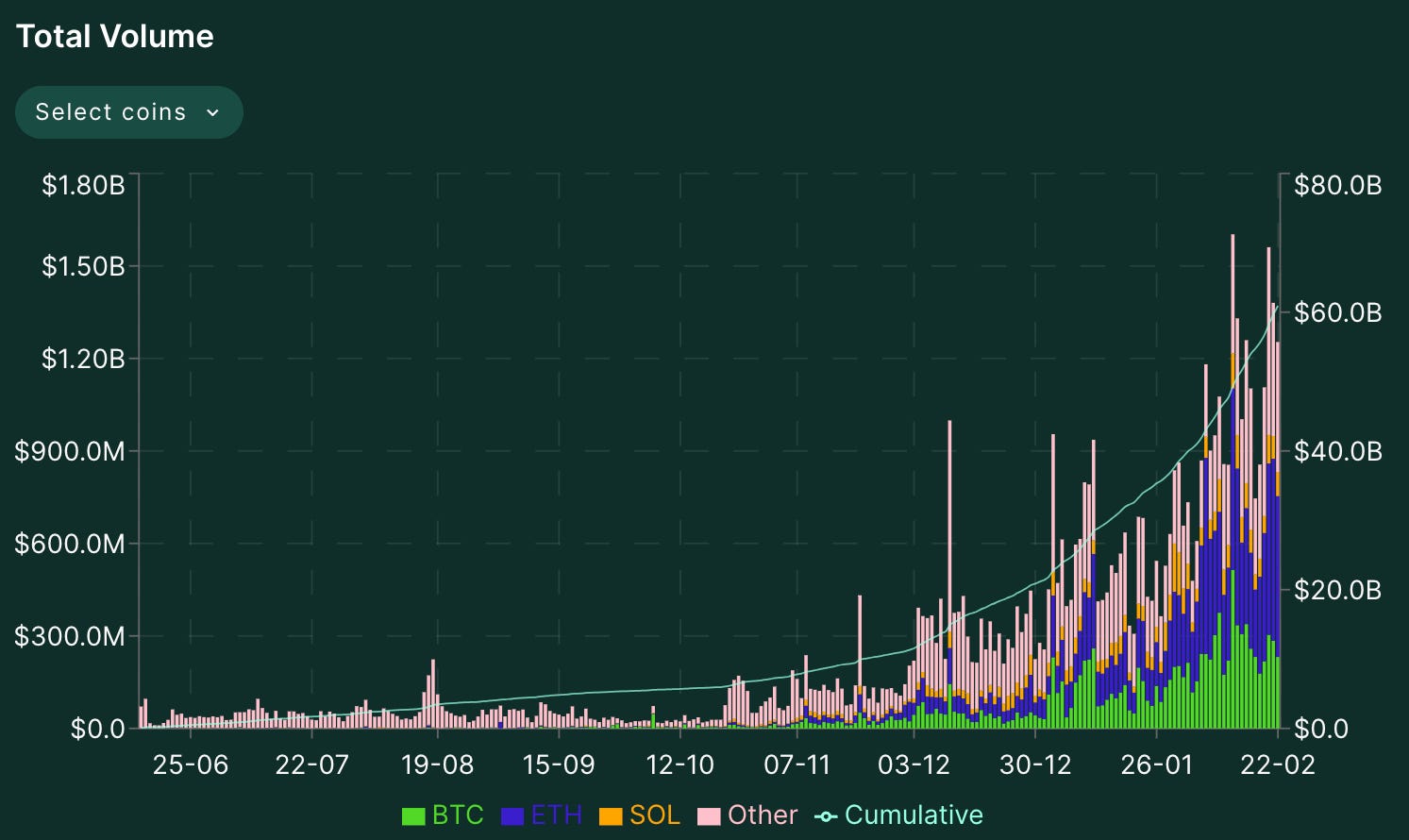

When combining improved market conditions along with Hyperliquid’s advantageous features listed in the Solution section above, Hyperliquid is growing at a rapid pace. The protocol has achieved $23.7b of its cumulative $55.6b trading volume (42.6%) within the last 30 days, attracting approximately 600-1,000 new users per day. [21]

Figure 5: Daily notional trading volume on Hyperliquid [22]

6. Market size

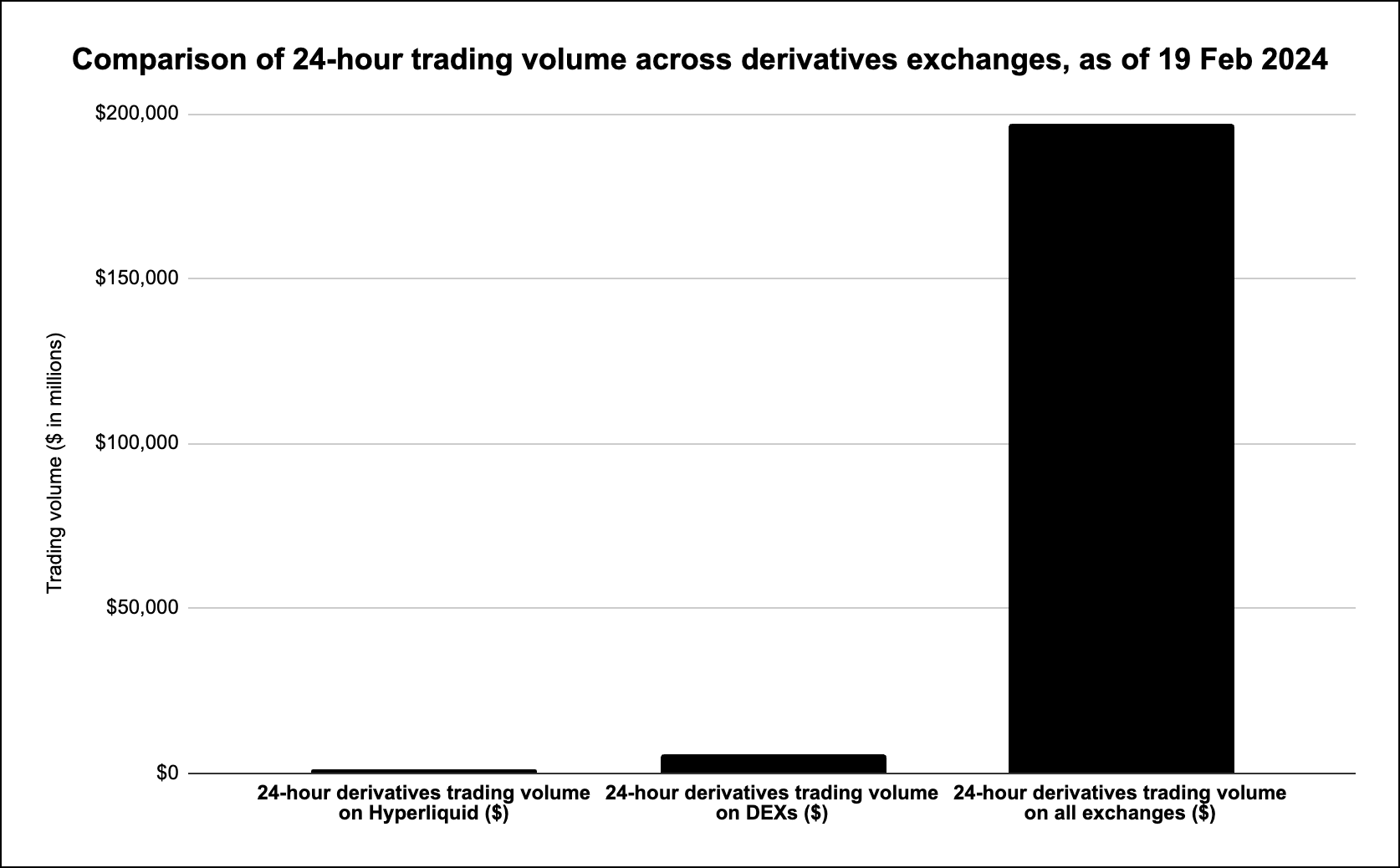

On Feb 19, 2024, over $197b in perpetual trading volume was facilitated across CEXs and DEXs, where DEXs accounted for only $5.5b (2.8%) of this volume. [23][24] The vast majority of trading volume currently still occurs on CEXs, due to the ease of user onboarding, relatively low trading fees, and flexibility with advanced order types (i.e. stop loss, take profit).

Within the DEX sector, Hyperliquid currently holds approximately 15% market share, having facilitated just over $850m in trading volume over the same 24-hour period. [25]

Figure 6: Comparison of 24-hour trading volume across derivatives exchanges, as of 19 Feb 2024

7. Competition

Hyperliquid’s competitors can again be categorized into two main groups - DEXs and CEXs.

7.1 DEXs

dYdX is currently the market-leading perpetual DEX by trading volume, while GMX leads by fees generated due to their higher take rate. Although Hyperliquid still lags behind these market leaders on their respective metrics, it is worth noting that Hyperliquid is exhibiting a much more positive growth trajectory, partly aided by its points system that promises a future token airdrop.

7.2 CEXs

Binance and OKX are the major centralized competitors of Hyperliquid. CEXs drive significantly more volume than DEXs like Hyperliquid, due to the reasons mentioned in the Market Size section above.

Figure 7: Key metrics of Hyperliquid and major competitors dYdX, GMX, Binance, and OKX

8. Product

Hyperliquid is composed of three main product components: the Hyperliquid blockchain, the bridge (from Arbitrum to the Hyperliquid blockchain), and the API servers. In this section, we will focus more on the Hyperliquid blockchain as this is the main product that makes up the DEX itself, and a special product feature on Hyperliquid known as ‘vaults’.

8.1 Hyperliquid blockchain

The Hyperliquid DEX runs on its own application-specific L1 chain, specifically designed for a computationally intensive derivative exchange. The consensus mechanism uses a version of Tindermint, which has previously also been used for BNB Chain, Oasis Labs, and Terra. [30] The median latency of the system is measured at 0.2 seconds, allowing users fast and reliable trade executions. [31]

8.2 Hyperliquid vaults

One of Hyperliquid’s unique products is its vault system, which allows users to ‘copy-trade’ vault owners whenever user funds are deposited into the vault. Any user can create a vault, and users who have deposited funds earn yield from trading fees and profitable trades operated by the vault owner. The vault owners receive 10% of the total profit as a management fee. [32]

Figure 8: Hyperliquid vaults [33]

9. Business model

Figure 9: Hyperliquid’s business model

Traders on Hyperliquid pay trading fees whenever a leveraged position is opened, closed, or liquidated. At the moment, 100% of trading fees are allocated to Hyperliquid liquidity providers and the insurance fund (used to backstop liquidity providers in the case of bad debt). [34]

I anticipate that Hyperliquid will likely begin to take a cut of trading fees as protocol revenue once the protocol has matured and turns its focus from achieving rapid adoption to growing earnings.

10. Team

The Hyperliquid team was initially founded by the pseudonymous Jeff and iliensinc in 2020, with a focus on crypto market-making. The team subsequently transitioned into creating their own DeFi protocol (Hyperliquid) in 2022, after they perceived the lack of a sophisticated DEX on the market. Their previous work experience includes roles at Citadel and Airtable, with educational backgrounds from Harvard, Caltech, MIT, and Waterloo. [35]

11. Financials

Although Hyperliquid has not disclosed its fee intake, nor is this information available on other data analytics platforms, we can estimate this based on its trading volume and trading fee rates. Given that:

Hyperliquid introduced trading fees in June 2023 [36]

Hyperliquid has facilitated $55b in trading volume since June 2023 [37]

The average trading fee is approximately 0.025%. [38] This may fluctuate due to

discounted rates for traders with high volumes, but here we are taking 0.025% as the

average fee rate.

$55b * 0.025% = $13.8m in trading fees since June 2023

This is significantly lower than the $68.6m generated by competitor GMX over the same period, although both have facilitated similar trading volumes. [39] This can be attributed to Hyperliquid’s lower take rate, although Hyperliquid may begin to shift fees up as users become more loyal and acclimated to the Hyperliquid trading UX. In addition, as all fees are currently allocated to liquidity providers, there may be a boost in fees in the future to allow for value accrual to the unreleased token (i.e. protocol yield for token stakers) as is common in the sector.

It is important to note that Hyperliquid is currently allocating points to traders, which will result in a retroactive airdrop of Hyperliquid’s governance token on a pro-rata basis based on trading volume. This will most likely result in downward pressure on Hyperliquid’s token in the short-term as some early users sell off their allocation.

Hyperliquid has not taken any external funding, and will not be required to allocate a portion of its governance tokens to investors. [40] This implies that a larger portion of total Hyperliquid tokens are being allocated towards the team or the community via token incentives, relative to other similar projects. This also creates an uncommon market dynamic that may potentially be positive for long-term token prices, whereby large institutional investors are forced to buy from the secondary market (or over-the-counter purchases from large holders) to gain exposure.

Conclusion

Hyperliquid is a decentralized perpetual exchange built on its application-specific chain. Launched in 2022, Hyperliquid has facilitated $55.6b in trading volume, with $23.7b from the previous 30 days alone. The protocol is consistently within the top 5 DEXs by daily notional trading volume, surpassing longstanding competitors such as GMX and Vertex Protocol.

This rapid growth is likely boosted by promises of a token airdrop via a points system, which has encouraged traders to speculate on the platform. Nevertheless, it still lags behind the market-leading DEX dYdX and is dwarfed by CEXs such as Binance and OKX.

Overall, due to its strong growth trajectory, advantageous product features, and lack of token allocation to early investors/insiders, I would strongly consider investing in the Hyperliquid token once it has been released. However, it must be noted that there may be some short-term volatility immediately following the token release as users sell their airdrop.

References

BitMex, XBTUSD: https://blog.bitmex.com/why-xbtusd-is-a-superior-trading-product/

Token Terminal, Derivatives market sector:

DefiLlama - Derivatives: https://defillama.com/derivatives

CoinGecko - Derivatives Exchanges: https://www.coingecko.com/en/exchanges/derivatives

DefiLlama - Derivatives: https://defillama.com/derivatives

Wall Street Journal - FTX:

https://www.wsj.com/articles/ftx-says-8-9-billion-in-customer-funds-are-missing-c232f684

OKX - Proof of Reserves: https://www.okx.com/proof-of-reserves

GMX - Trading docs: https://gmxio.gitbook.io/gmx/trading

Binance - Trading fees: https://www.binance.com/en/fee/futureFee

OKX - Trading fees: https://www.okx.com/web3/dex-perp/test/market-info/fee

Token Terminal - Transactions per second:

https://tokenterminal.com/terminal/metrics/transactions-per-second

GMX - Trading: https://app.gmx.io/#/trade

dYdX - Trading: https://dydx.trade/?utm_source=dydx-website#/trade/ETH-USD

CoinGecko - OKX derivatives: https://www.coingecko.com/en/exchanges/okx_swap

CoinGecko - Binance derivatives:

DefiLlama - Derivatives: https://defillama.com/derivatives

Hyperliquid - Fees docs: https://hyperliquid.gitbook.io/hyperliquid-docs/trading/fees

Hyperliquid - Fees docs: https://hyperliquid.gitbook.io/hyperliquid-docs/trading/fees

Hyperliquid - NFT index perp article:

CoinGlass - BTC open interest and volume: https://www.coinglass.com/pro/futures/Cryptofutures

Hyperliquid - Stats: https://stats.hyperliquid.xyz/

Hyperliquid - Stats: https://stats.hyperliquid.xyz/

CoinGecko - Derivatives Exchanges: https://www.coingecko.com/en/exchanges/derivatives

DefiLlama - Derivatives: https://defillama.com/derivatives

Hyperliquid - Stats: https://stats.hyperliquid.xyz/

DefiLlama - Derivatives volumes: https://defillama.com/derivatives

CoinGlass - Exchanges: https://www.coinglass.com/exchanges

CoinGecko - DYDX token: https://www.coingecko.com/en/coins/dydx-chain

CoinGecko - GMX token: https://www.coingecko.com/en/coins/gmx

Tendermint: https://tendermint.com/

Hyperliquid - Hyperliquid L1 docs:

https://hyperliquid.gitbook.io/hyperliquid-docs/technical-overview/hyperliquid-l1

Hyperliquid - Vaults docs: https://hyperliquid.gitbook.io/hyperliquid-docs/vaults

Hyperliquid - Vaults: https://app.hyperliquid.xyz/vaults

Hyperliquid - Fees docs: https://hyperliquid.gitbook.io/hyperliquid-docs/trading/fees

Hyperliquid - Core contributors docs:

https://hyperliquid.gitbook.io/hyperliquid-docs/about-hyperliquid/core-contributors

Hyperliquid - Fees docs: https://hyperliquid.gitbook.io/hyperliquid-docs/trading/fees

Hyperliquid - Stats: https://stats.hyperliquid.xyz/

Hyperliquid - Fees docs: https://hyperliquid.gitbook.io/hyperliquid-docs/trading/fees

Token Terminal - GMX dashboard: https://tokenterminal.com/terminal/projects/gmx

Hyperliquid - Core contributors docs:

https://hyperliquid.gitbook.io/hyperliquid-docs/about-hyperliquid/core-contributors